Building a Winning Investment Portfolio: A UK Strategic Framework

Table of Contents

Investment portfolios represent more than collections of assets—they’re strategic frameworks designed to achieve specific financial objectives while managing risk. For UK business owners, marketing managers, and decision-makers, understanding portfolio construction isn’t just about personal wealth management. The principles that drive successful investment strategies mirror those required for business growth: calculated risk-taking, diversification, continuous optimisation, and data-driven decision-making.

This comprehensive guide explores investment portfolio strategy through a practical lens, examining how the same analytical thinking that builds profitable portfolios can inform business development decisions. Whether you’re considering how to allocate marketing budgets, diversify revenue streams, or structure long-term business investments, the frameworks presented here offer transferable insights. We’ll examine portfolio construction, risk management, and performance measurement while drawing parallels to digital strategy and business growth—where ProfileTree supports organisations across Northern Ireland, Ireland, and the UK.

Understanding Investment Portfolios and Their Strategic Purpose

Investment portfolios serve as structured frameworks for capital allocation, designed to balance risk against expected returns over specific time horizons. At their core, portfolios represent deliberate choices about resource deployment—a concept equally applicable to financial markets and business strategy. As companies allocate budgets across different marketing channels or product lines, investors distribute capital across various asset classes to achieve optimal outcomes.

The fundamental concept behind any investment is straightforward: committing resources today for greater value tomorrow. This requires compensation for three primary factors: the time value of money, the erosion caused by inflation, and the uncertainty inherent in any venture. These same principles govern business investments, whether you’re developing a new website, implementing AI solutions, or expanding into new markets.

What Constitutes an Investment Portfolio

A financial portfolio comprises all your investment holdings—stocks, bonds, property, cash equivalents, and alternative assets—structured to meet specific objectives. Think of it as a diversified basket of opportunities, each selected for potential contribution to your goals. The portfolio’s aggregate characteristics—expected return, risk profile, and liquidity—emerge from how these components interact.

For business leaders, this concept extends beyond traditional investments. Your company’s “portfolio” might include your digital assets (website, content library, social media presence), service offerings, client base, and intellectual property. Understanding how these elements work together—and how to optimise their collective performance—requires the same strategic thinking that drives investment portfolio management.

The Nature of Investment Returns

Returns from investment portfolios manifest in various forms. Equities generate returns through capital appreciation and dividends. Bonds provide regular coupon payments plus return of principal. Property investments offer rental income and potential value appreciation. Each return type carries different tax implications, risk characteristics, and timing considerations—particularly relevant in the UK context where tax efficiency significantly impacts net returns.

According to Vanguard’s research, portfolios with diversification across asset classes demonstrate approximately 20% lower volatility than single-asset portfolios. This reduction in volatility doesn’t necessarily mean lower returns—rather, it represents more stable, predictable growth patterns. This principle translates directly to business revenue diversification: companies with multiple service lines or revenue streams typically experience more stable growth than those dependent on a single offering.

Investment Categories and Asset Classes

Investment opportunities fall into several broad categories, each serving different purposes within a portfolio:

Ownership Investments involve acquiring assets with appreciation potential. This category includes equities (stocks), real estate, businesses, and commodities. The strategy centres on identifying undervalued assets, acquiring them, and selling when their market value exceeds the purchase price. This parallels strategic acquisitions, brand building, or developing proprietary technology that appreciates in the business world.

Lending Activities generate returns through interest payments. Bonds, certificates of deposit, peer-to-peer lending, and savings accounts fall into this category. These typically offer lower returns than ownership investments but with correspondingly lower risk. Companies engage in similar activities when they extend payment terms to reliable clients or invest working capital in short-term instruments.

Alternative Investments encompass strategies that don’t fit traditional categories: foreign exchange trading, derivatives, private equity, and hedge fund strategies. These often require specialist knowledge and carry higher risk profiles. For businesses, alternatives might include experimental marketing channels, emerging technologies, or innovative service delivery models.

Modern Portfolio Theory and Strategic Diversification

Harry Markowitz’s Modern Portfolio Theory, developed in the 1950s, revolutionised investment thinking by demonstrating mathematically that diversification could reduce risk without sacrificing returns. The theory rests on two key insights: investors naturally seek maximum returns for minimum risk, and risk can be minimised through carefully structured diversification.

This isn’t theoretical abstraction—it’s practical wisdom with direct business applications. Research from the Journal of Financial Planning shows that portfolios optimised using Modern Portfolio Theory achieve the same expected returns with 15-20% less risk than non-optimised portfolios. Similarly, businesses that diversify their service offerings, geographic markets, or client sectors typically experience more resilient growth.

“The principles that govern successful investment portfolios apply equally to business strategy,” notes Ciaran Connolly, Director of ProfileTree. “Whether you’re allocating financial capital or marketing budgets, the fundamentals remain constant: understand your objectives, measure your risk tolerance, diversify intelligently, and optimise continuously based on performance data.”

Strategic Asset Allocation and Portfolio Construction

Asset allocation—dividing your portfolio among different investment categories—represents the most crucial decision affecting long-term returns. Brinson, Hood, and Beebower found that asset allocation explains over 90% of portfolio return variability over time, dwarfing the impact of security selection or market timing. This makes getting your allocation right absolutely fundamental to investment success.

The allocation decision involves balancing several competing factors: your time horizon, risk tolerance, income requirements, tax situation, and specific financial objectives. These same considerations apply when businesses allocate resources across different initiatives—dividing marketing budgets between SEO, content marketing, and paid advertising, or balancing investment between existing service refinement and new offering development.

Determining Your Risk Tolerance and Investment Horizon

Risk tolerance combines psychological comfort with financial capacity. Can you emotionally withstand significant temporary losses? More importantly, can your financial situation absorb them without derailing your plans? These questions demand honest answers before constructing any portfolio.

Your investment horizon—the timeframe until you access your capital—dramatically influences appropriate risk levels. Longer horizons permit accepting higher volatility in exchange for potentially superior returns. Research from Morningstar indicates that investors whose portfolios align with their risk tolerance and time horizon achieve 1-2% higher average annual returns than those with misaligned portfolios.

For businesses, the parallel is clear. Marketing investments in SEO or content creation require longer timeframes to generate returns compared to paid advertising, but often deliver superior long-term value. Understanding your business’s risk tolerance—financial capacity, competitive positioning, and stakeholder expectations—should guide resource allocation decisions.

Core Portfolio Building Blocks

Equities offer growth potential but with significant volatility. Historically, UK equities have delivered average annual returns around 7-9% after inflation over long periods, though with substantial year-to-year variation. Younger investors or those with longer time horizons typically allocate larger portions to equities, accepting short-term volatility for long-term growth potential.

Fixed-income investments—primarily bonds—provide more stable, predictable returns. UK government bonds (gilts) offer security backed by sovereign credit, while corporate bonds provide higher yields in exchange for accepting corporate default risk. Bond allocations typically increase as investors approach their financial goals, prioritising capital preservation over growth.

Alternative Assets including property, commodities, and private investments, can provide diversification benefits, as their returns often show low correlation with traditional stocks and bonds. However, these typically require larger minimum investments, have lower liquidity, and may involve higher costs.

Cash and Cash Equivalents provide liquidity and stability but generate minimal real returns, particularly in low-interest-rate environments. They serve important roles as emergency reserves and tactical opportunities to deploy capital when attractive investments emerge.

The Diversification Imperative

“Don’t put all your eggs in one basket” encapsulates diversification’s essential wisdom. But effective diversification requires more than simply owning multiple investments—it demands selecting assets with low correlation, meaning they don’t all move together. When properly diversified, portfolio losses in one area are offset by stability or gains elsewhere.

Fidelity’s research demonstrates that adding international stocks to a UK-focused portfolio can lower total volatility by 3 percentage points or more. During the 2008 financial crisis, DALBAR analysis showed that globally diversified portfolios suffered maximum drawdowns of approximately 26%, compared to 47% for concentrated portfolios—a difference that could devastate financial plans, versus causing temporary discomfort.

This principle extends directly to business strategy. Companies relying on a single client, market, or service line face existential risk if that revenue source falters. Smart diversification—across client sectors, geographic markets, or complementary services—provides resilience against market disruptions.

Age-Based and Goal-Based Allocation Strategies

Traditional guidance suggests subtracting your age from 100 to determine equity allocation percentage (100 minus 40 years equals 60% equities). Whilst overly simplistic, this heuristic captures an important truth: reducing volatility becomes increasingly crucial as you approach financial goals.

Goal-based investing offers a more sophisticated approach, structuring portfolios around specific objectives with defined timeframes and required returns. Short-term goals (under five years) demand conservative allocations prioritising capital preservation. Medium-term goals (5-15 years) permit balanced approaches. Long-term goals (over 15 years) can accept higher volatility for growth potential.

Business strategy benefits from similar goal-based thinking. Short-term revenue targets might require tactical paid advertising investments with immediate returns. Building long-term brand authority demands patient investment in content marketing, SEO, and thought leadership—initiatives that compound value over years rather than generating immediate returns.

UK Tax-Efficient Investment Structures

The UK offers several tax-advantaged investment vehicles that should feature prominently in any portfolio strategy. Individual Savings Accounts (ISAs) allow up to £20,000 annual investment (2024/25 tax year) with tax-free growth and withdrawals. Self-Invested Personal Pensions (SIPPs) provide tax relief on contributions whilst deferring taxation until retirement withdrawals begin.

Understanding these structures matters because tax efficiency dramatically impacts net returns over time. A portfolio generating 7% annual returns but losing 20% to taxes nets just 5.6%—a significant difference compounded over decades. Similarly, businesses must structure operations tax-efficiently, whether claiming R&D credits for AI implementation or optimising VAT treatment of digital services.

The Business Asset Disposal Relief (formerly Entrepreneurs’ Relief) offers preferential capital gains treatment when selling qualifying business assets—relevant context when considering how business investments fit within broader wealth strategies. For company directors and entrepreneurs, coordinating business and personal investment strategies often yields superior outcomes compared to treating them separately.

UK Market Dynamics and Regional Business Considerations

The UK market presents unique characteristics that affect both investment and business strategies. London’s position as a global financial centre concentrates specific opportunities while creating higher costs. Regional variations across England, Scotland, Wales, and Northern Ireland affect property values, labour markets, and business conditions.

Understanding local dynamics proves crucial for businesses operating across these regions. An SEO strategy targeting “Belfast web design” requires different approaches than targeting London markets, reflecting different competitive landscapes, search volumes, and commercial intent patterns. Similarly, content marketing strategies must consider regional terminology preferences, industry concentrations, and local business networks.

Digital Asset Investment and Business Growth

While traditional portfolio theory focuses on financial assets, forward-thinking business leaders increasingly recognise digital assets as critical components requiring strategic investment and management. Your website, content library, social media presence, and proprietary technology represent valuable assets that appreciate over time when properly maintained and developed.

A well-designed, properly optimised website functions as an appreciating business asset. Unlike physical property requiring ongoing maintenance costs, digital assets can generate increasing returns with relatively modest ongoing investment. According to ProfileTree’s client data, businesses investing consistently in SEO and content marketing typically see compound traffic growth of 20-30% annually—returns rivalling traditional investment returns while simultaneously driving business growth.

Video content represents another high-value digital asset class. A well-produced video explaining your services or demonstrating expertise generates value—views, engagement, and conversions—long after production costs are sunk. Like bonds providing recurring income, quality content generates ongoing organic traffic and leads without additional media spend. <div id=”risk-management-techniques”></div>

Risk Management and Portfolio Optimisation Strategies

Risk management separates successful long-term investors from speculators. Whilst accepting appropriate risk is necessary for generating returns, managing that risk through deliberate strategies protects capital and prevents emotional decision-making during market turbulence.

Understanding and Measuring Portfolio Risk

Risk manifests in multiple dimensions beyond simple volatility. Standard deviation measures how much returns fluctuate around their average—a higher standard deviation indicates greater uncertainty. Maximum drawdown captures the most significant peak-to-trough decline, revealing worst-case historical scenarios. Beta measures sensitivity to overall market movements, indicating how much a portfolio might decline during broad market downturns.

For UK investors, currency risk deserves particular attention when holding international assets. Sterling fluctuations against the dollar, euro, or other currencies add uncertainty to foreign investments. Whilst this can work favourably, it introduces complexity requiring active management or acceptance as part of overall risk exposure.

Business risk manifests similarly across multiple dimensions: revenue concentration risk—dependence on a few clients—parallels portfolio concentration risk. Operational risk from technology failures or key person dependencies mirrors liquidity risk in portfolios. Strategic risk from competitive disruption resembles market risk in investments. Recognising these parallels helps business leaders apply investment risk management principles to operational strategy.

Rebalancing Strategies and Discipline

Portfolio drift occurs naturally as different assets generate varying returns, causing allocations to deviate from targets. A portfolio starting at 60% equities / 40% bonds might drift to 70% / 30% after strong equity performance, increasing risk exposure beyond intended levels.

Rebalancing restores target allocations by selling outperforming assets and buying underperformers—essentially automating the “buy low, sell high” discipline. Academic studies show that strategic rebalancing boosts cumulative returns by approximately 0.4% annually while reducing volatility. Vanguard and Morningstar research indicate that automated rebalancing strategies generate 0.30% additional annual returns compared to never rebalancing.

Most experts recommend rebalancing at least annually, or when allocations skew 5-10% from targets. Threshold-based rebalancing (triggered by allocation drift) often outperforms calendar-based approaches, though it requires more monitoring. For taxable accounts, consider rebalancing primarily within tax-advantaged accounts to minimise capital gains tax implications.

Business strategy demands similar rebalancing discipline. Marketing budgets naturally drift toward comfortable, familiar channels. Service offerings expand incrementally without strategic evaluation. Client portfolios concentrate on historically strong sectors. Regular strategic reviews—quarterly or semi-annually—allow deliberate reallocation toward the highest-return opportunities, pruning underperforming initiatives before they consume disproportionate resources.

Avoiding Emotional Decision-Making and Behavioural Traps

Behavioural finance research reveals that psychological biases often derail otherwise sound investment strategies. Loss aversion causes investors to sell winning positions too quickly, while holding losers too long. Recency bias leads to chasing recent strong performers just before reversion to the mean. Confirmation bias encourages seeking information supporting existing positions rather than challenging them objectively.

Panic selling during market declines proves particularly destructive. Markets inevitably experience corrections and bear markets—temporary declines that long-term investors must weather. Selling during these periods locks in losses and often causes investors to miss subsequent recoveries. Data from Betterment shows that investors who maintained discipline during 2020’s COVID-19 market crash recovered fully within months, whilst those who sold near the bottom took years to recover.

Businesses fall prey to similar behavioural traps. The sunk cost fallacy causes failing projects to continue because of prior investment. Availability bias leads to overweighting recent client feedback versus comprehensive data. The herd mentality drives the adoption of trendy tactics without strategic justification. Establishing decision frameworks—data-driven evaluation criteria applied consistently—helps overcome these natural psychological tendencies.

Tax-Loss Harvesting and Efficiency Strategies

Tax-loss harvesting involves selling investments trading below purchase price to realise losses for tax purposes, then replacing them with similar (but not identical) investments to maintain market exposure. This strategy effectively converts temporary portfolio losses into permanent tax benefits, improving after-tax returns by 0.3-0.5% annually according to research.

UK investors must navigate wash sale rules preventing the repurchase of identical securities within 30 days, while claiming the loss. However, you can immediately purchase similar but not identical investments—for example, selling one FTSE 100 tracker and buying another from a different provider. Within ISAs and pensions, this strategy offers no benefit since these accounts already provide tax-free growth.

Businesses employ similar tax efficiency strategies: timing discretionary spending to optimise tax years, structuring service delivery to maximise allowable deductions, or claiming reliefs like R&D tax credits. As tax-efficient investing improves net portfolio returns, tax-efficient business operations improve bottom-line profitability without increasing revenue. <div id=”performance-measurement”></div>

Measuring Portfolio Performance and Continuous Optimisation

You cannot improve what you don’t measure. Rigorous performance measurement enables evidence-based optimisation, identifying what works and what doesn’t. This applies equally to investment portfolios and business strategies—both demand systematic tracking, honest evaluation, and disciplined adjustment based on results.

Establishing Appropriate Benchmarks

Performance measurement requires context. Gaining 5% sounds positive until you learn that comparable investments returned 8%. Benchmarks provide this context, answering the question, “How did I perform relative to what I could have achieved?”

Benchmarks should match your portfolio’s characteristics. A UK equity-heavy portfolio might benchmark against the FTSE All-Share Index. A globally diversified portfolio might use the MSCI World Index. A balanced portfolio might benchmark against a blended index matching your target allocation—for example, 60% FTSE All-Share plus 40% UK Gilt Index.

Custom benchmarks often prove meaningful, reflecting your specific allocation targets and objectives. Rather than comparing against a single index, construct a weighted benchmark mirroring your intended allocation across equities, bonds, alternatives, and cash. This reveals whether your active decisions (security selection, tactical tilts, timing) added value versus simply holding index funds matching your allocation.

Business performance measurement demands similarly thoughtful benchmarking. Comparing your website traffic growth against industry averages reveals whether you’re gaining or losing competitive ground. Benchmarking your SEO visibility against direct competitors identifies gaps and opportunities. Measuring client acquisition costs against customer lifetime value indicates whether your marketing investment generates positive returns.

Calculating Risk-Adjusted Returns

Absolute returns tell an incomplete story without considering the risk to achieve them. Risk-adjusted metrics provide a fuller context:

The Sharpe Ratio measures excess return (return above the risk-free rate) per unit of volatility. Higher Sharpe ratios indicate superior risk-adjusted performance—you’re getting more return per unit of risk accepted. A Sharpe ratio above 1.0 generally indicates good risk-adjusted performance, whilst above 2.0 is excellent.

The Sortino Ratio refines the Sharpe by considering only downside volatility. Psychologically, losses matter more than gains, so measuring risk-adjusted return against downside volatility better captures investor experience. This proves particularly useful for evaluating strategies that limit downside while capturing upside.

Alpha measures returns exceeding what your benchmark would predict given your portfolio’s risk characteristics. Positive alpha indicates value added through security selection or strategy beyond simply accepting market risk. However, generating consistent positive alpha proves exceptionally difficult—most active managers fail to do so after accounting for fees.

For businesses, risk-adjusted thinking applies directly to strategic decisions. A marketing channel generating £10,000 monthly revenue deserves different evaluation depending on whether that revenue varies wildly (high risk) or arrives predictably (low risk). High-risk revenue streams demand higher returns to justify acceptance versus stable, predictable channels.

Attribution Analysis and Understanding Return Drivers

Attribution analysis breaks down portfolio returns into components: asset allocation effect, security selection effect, and interaction effect. This reveals whether your returns came primarily from broad allocation decisions or specific security choices within asset classes.

For most investors, asset allocation drives most returns. Brinson’s studies found that over 90% of return variability stems from allocation decisions rather than security selection. This finding strongly argues for focusing primarily on getting allocation rights and using low-cost index funds to implement them rather than spending excessive time trying to identify superior individual securities.

Business attribution analysis follows similar logic. Did revenue growth come from existing client expansion or new customer acquisition? Did website traffic increase from improved rankings for existing keywords or expansion into new keyword territories? Attribution analysis identifies which strategies actually drive results versus those receiving credit coincidentally.

ProfileTree’s digital strategy approach emphasises this attribution thinking. When clients see website traffic increase after simultaneous SEO improvements, content expansion, and paid advertising campaigns, attribution analysis reveals which initiatives drove results—critical information for future resource allocation decisions.

Continuous Optimisation and Strategic Adjustments

Portfolio management is never “set and forget.” Markets evolve, personal circumstances change, and new opportunities emerge. Successful investors review portfolios regularly—at least annually, quarterly for more active approaches—evaluating whether current allocations align with objectives and circumstances.

This doesn’t mean constant tinkering. Trading too frequently increases costs and taxes, often reflecting emotional reactions rather than strategic thinking. Instead, establish regular review cadences: quarterly monitoring for drift and rebalancing needs, annual comprehensive strategic reviews evaluating whether fundamental allocation targets remain appropriate.

Between scheduled reviews, maintain discipline. Unless circumstances change dramatically—job loss, inheritance, health crisis—avoid reactive changes based on market movements or news headlines. Your allocation strategy should already incorporate expectations for market volatility. Reacting to normal market behaviour suggests either your allocation doesn’t match your risk tolerance or you’re falling into behavioural traps.

Business strategy demands identical discipline. Quarterly reviews should assess performance against objectives, evaluate resource allocation effectiveness, and make tactical adjustments. Annual strategic planning should revisit fundamental business direction, competitive positioning, and significant investment priorities. Between reviews, maintain strategic focus rather than chasing every new tactic or reacting to competitive moves without strategic evaluation.

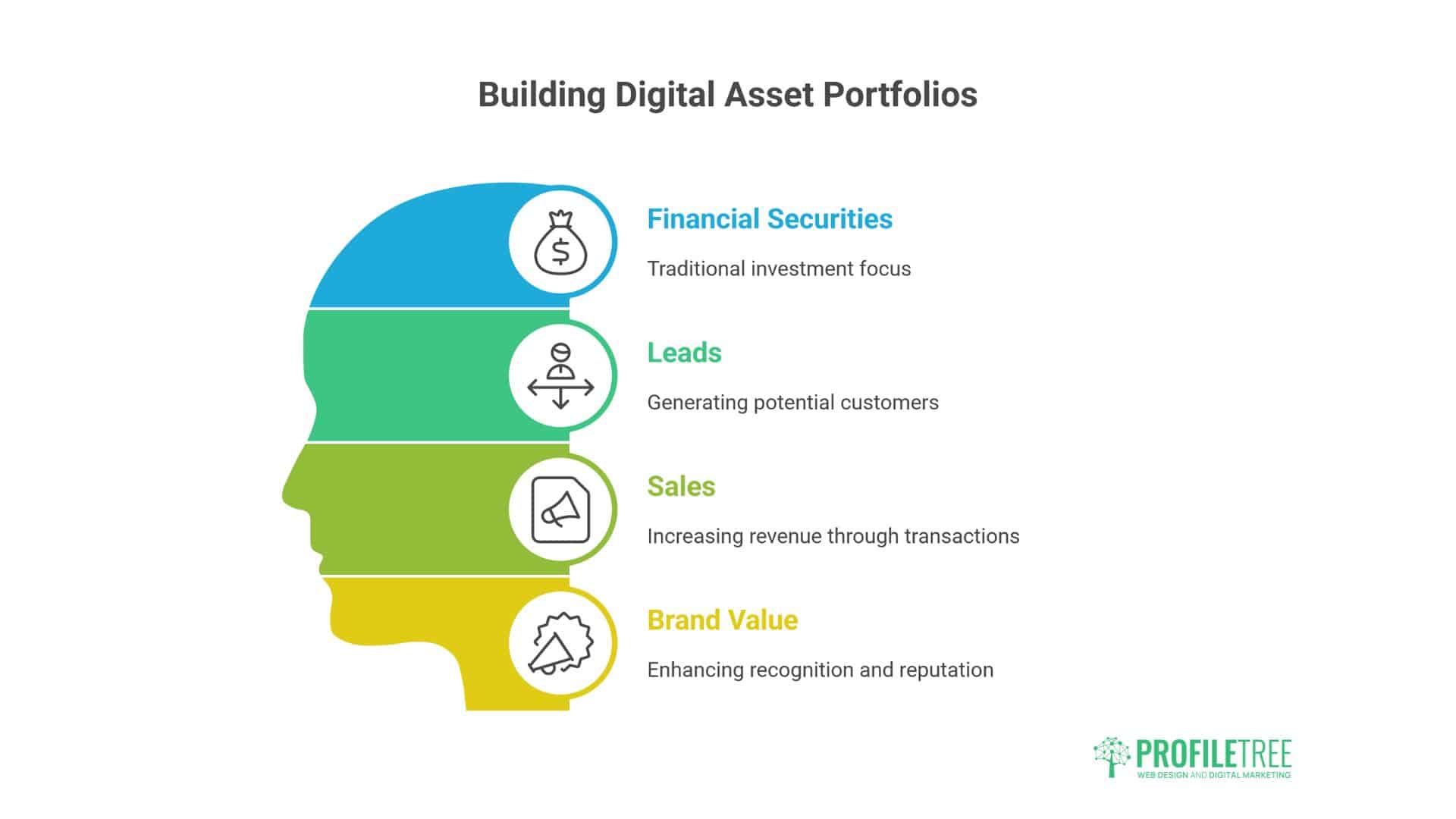

Building Digital Assets as Portfolio Components

While traditional investment portfolios focus on financial securities, businesses must simultaneously build portfolios of digital assets that appreciate over time and generate returns through leads, sales, and brand value.

Website Development as Capital Investment

Your website represents a capital investment requiring upfront resources but generating ongoing returns. A well-designed, properly optimised website appreciates as it accumulates authority, rankings, and traffic. Unlike depreciating physical assets, digital assets can increase in value indefinitely with appropriate maintenance and development.

Consider website development through a portfolio lens: what return do you expect relative to investment? A £15,000 website generating 50 qualified leads monthly at £100 value each creates £5,000 monthly return—a 40% monthly return on initial investment, or 480% annualised. Few traditional investments approach this return potential.

However, like any investment, websites require ongoing management. Technical maintenance, security updates, content additions, and SEO optimisation represent the equivalent of portfolio rebalancing and optimisation. Neglecting these maintenance activities causes digital asset depreciation as competitors advance, search algorithms evolve, and technology becomes outdated.

ProfileTree’s web design approach treats websites as strategic business assets requiring professional architecture, not just attractive design. We focus on performance, conversion optimisation, and organic visibility—the factors that drive measurable business returns from this critical digital investment.

Content Marketing as Compound Growth Strategy

Content marketing functions similarly to dividend reinvestment in equity portfolios. Each article published represents an asset producing ongoing returns through organic traffic. As your content library grows, aggregate returns compound—new content adds incrementally whilst existing content continues performing.

Research from HubSpot indicates companies publishing 16+ monthly blog posts generate 4.5 times more leads than those publishing 0-4 monthly. This isn’t linear scaling—it’s compound growth from an expanding asset base. Like portfolio compound returns, content marketing returns accelerate as your asset base grows, assuming quality remains high.

Content portfolio diversification matters equally. Focusing exclusively on a single topic creates concentration risk—algorithm changes, market shifts, or competitive dynamics can devastate traffic. Diversifying content across multiple relevant topics, formats (articles, videos, infographics), and keyword targets provides resilience while maximising total traffic potential.

However, content quality matters immensely. Low-quality content represents the equivalent of junk bonds—superficially attractive yields that fail to deliver due to fundamental problems. Google’s algorithms increasingly prioritise expertise, authoritativeness, and trustworthiness. Investing in quality content production generates sustainable long-term returns, while cheap, thin content delivers diminishing returns as algorithms evolve.

Video Production and YouTube Strategy

Video content offers particularly high return potential in current digital landscapes. YouTube is the world’s second-largest search engine, with video content often ranking prominently in Google search results. A single well-optimised video can generate thousands of views and dozens of leads over its lifetime.

Video production requires a higher upfront investment than written content, but superior engagement and conversion rates often justify this investment. According to Wyzowl research, 84% of consumers are convinced to purchase after watching a brand’s video. Videos also offer remarkable longevity—relevant, evergreen video content continues generating views and value years after production.

Building a video content portfolio follows similar strategic principles to financial portfolios: diversify across topics and formats, maintain consistent quality standards, optimise for discovery through proper tagging and descriptions, and analyse performance to identify what resonates with your target audience.

ProfileTree’s video production services focus on strategic video assets that generate measurable business returns, not attractive content. We structure video strategies as long-term asset accumulation programmes, building content libraries that increase value over time through expanding reach and authority.

SEO as Long-Term Growth Investment

Search engine optimisation represents perhaps the most apparent parallel to a traditional investment strategy. SEO requires patient capital investment—months typically pass before significant returns materialise. However, once established, organic search visibility generates ongoing returns without direct costs per visitor, unlike paid advertising’s transactional model.

SEO investment diversification matters critically. Ranking for a single keyword creates a dangerous concentration risk—algorithm updates, competitive pressure, or search trend shifts can instantly eliminate traffic. Diversified SEO strategies target multiple keywords across different search intents (informational, commercial, transactional), providing resilience and multiple traffic pathways.

Technical SEO, content development, and link building are the primary SEO investment components, analogous to different asset classes. Technical SEO provides the foundation enabling search visibility. Content development creates the asset base, generating rankings and traffic. Link building establishes authority and competitive positioning. Balanced investment across all three generates optimal long-term returns.

Research demonstrates that businesses investing consistently in SEO over 12+ months typically see compound traffic growth of 20-30% annually, with rankings and visibility continuing to strengthen over time. This patient’s strategic approach dramatically outperforms tactical, campaign-based marketing, which generates temporary spikes without sustainable growth.

Taking Action: Your Portfolio Implementation Plan

Understanding portfolio principles matters only when converted into action. Please describe your current situation: list all existing investments, their values, and asset class allocations. Calculate your overall allocation and compare it to your target based on your risk tolerance and time horizon.

If starting fresh, open appropriate accounts: a Stocks and Shares ISA for tax-efficient investing and potentially an SIPP for pension savings. Before committing, compare platform fees, fund selections, and provider user experience.

Select investments based on your asset allocation targets. For most investors, a globally diversified portfolio built from 3-5 low-cost index funds provides optimal simplicity: a UK equity index fund, an international equity index fund, a UK bond index fund, and potentially a small alternatives allocation.

Establish automatic investment processes where possible. Monthly automatic investments implement pound-cost averaging systematically, removing emotional decision-making. Even modest amounts compound substantially—£300 monthly invested at 7% annual returns grows to over £360,000 after 30 years.

Document your investment policy: target allocation, rebalancing triggers, and circumstances justifying strategic changes. This written policy provides discipline during stressful market periods. Review annually to confirm alignment with your circumstances.

Business leaders should apply identical systematic thinking to digital asset investment. Allocate specific budgets to website development, content creation, SEO, and video production. Establish regular review cadences, evaluate returns, and maintain implementation discipline.

FAQs

How often should I rebalance my investment portfolio?

Most experts recommend rebalancing at least annually or when asset allocations drift 5-10% from targets. Threshold-based rebalancing (triggered by allocation drift) often outperforms calendar-based approaches, though it requires more monitoring. Within taxable accounts, consider rebalancing primarily in tax-advantaged accounts to minimise capital gains tax implications.

What’s the best asset allocation for my investment portfolio?

Optimal allocation depends on your risk tolerance, time horizon, and objectives. A common starting point is 60% equities and 40% bonds, adjusted based on circumstances. Younger investors or those with higher risk tolerance might allocate 80% or more to equities, while conservative investors or those approaching financial goals might hold 40% or less.

How many stocks should I hold in my portfolio?

Research suggests that 12-20 individual stocks provide adequate diversification for concentrated portfolios. However, holding individual stocks requires research, monitoring, and risk management, which most investors lack the expertise for. Low-cost index funds provide superior diversification (hundreds or thousands of holdings) with minimal effort, making them appropriate for most investors.

Should I include international stocks in my portfolio?

Yes, allocating 20-40% to international equities typically reduces portfolio volatility through diversification while providing exposure to global growth opportunities. UK equities represent just 4% of global market capitalisation, making purely domestic portfolios significantly under-diversified relative to global opportunity sets.