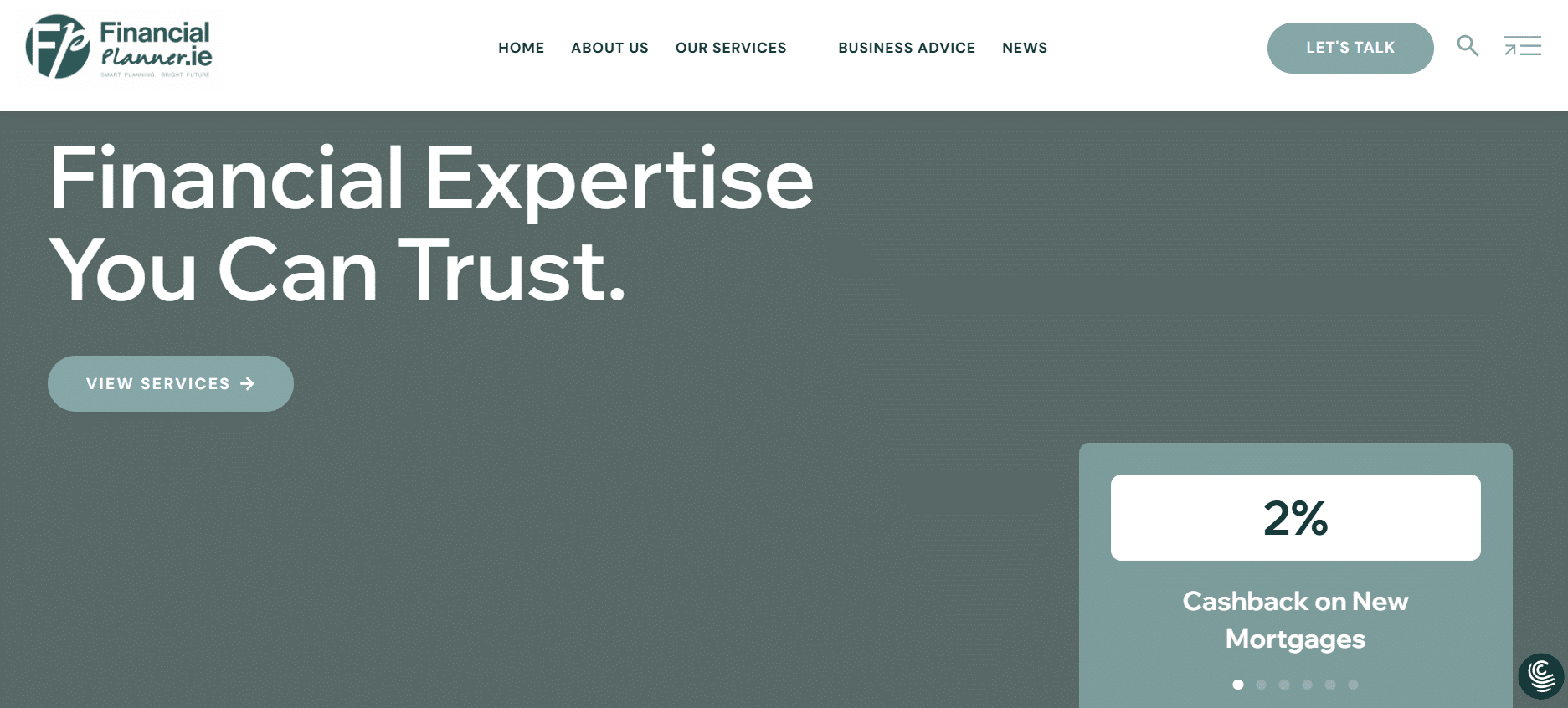

ProfileTree, a Belfast-based web design and digital marketing agency, builds professional websites for financial planning and regulated financial services businesses across Ireland and Northern Ireland. This case study covers a full WordPress website build for Financial Planner.ie, a Co. Kildare advisory firm with more than 25 years trading, covering SEO-optimised service pages, interactive financial calculators, and a lead-generating site structure.

The Challenge Financial Planning Businesses Face Online

Financial services are one of the most trust-dependent industries online. A potential client searching for mortgage advice, retirement planning, or business insurance is not going to pick up the phone to a firm whose website looks out of date, has no clear service structure, and gives no visible indication of experience or credibility. That is the core problem we see repeatedly when financial advisory businesses come to us at ProfileTree.

Most of these firms have built strong reputations over years of trading. They have satisfied clients, regulated advisors, and deep expertise across multiple financial services areas. But their websites were often built years ago, have never been properly optimised for search, and are structured around what the firm does rather than what their clients are searching for.

There are three specific issues that come up in almost every discovery session with a financial advisor. First, the service pages are too thin. A single page that lists financial planning, mortgage advice, retirement planning, and business insurance as four bullet points is not going to rank for any of those services individually. Each deserves its own dedicated page with proper content, keyword focus, and calls to action.

Second, the site cannot be managed internally. Financial advisors operate in a regulated environment where rates, products, and guidance change regularly. If updating the website requires calling a developer, those updates simply do not happen. The site becomes stale, search engines notice, and rankings drop.

Third — and this is the one that costs the most in missed enquiries — most financial advisor websites have no mechanism for capturing leads from visitors who are not quite ready to call. No calculators, no downloadable guides, no quote tools. Visitors arrive, read a little, and leave. For more on how professional services firms can structure their digital presence to generate consistent enquiries, see our overview of professional services digital strategy at digital marketing in Northern Ireland.

About Financial Planner.ie: The Project

Financial Planner.ie is a financial advisory firm based in Co. Kildare, Ireland, with a team of four professionals: Brendan (CEO and Financial Advisor), Eileen (Operations Manager), Trish (Managing Director and Mortgage Specialist), and James (Office Administrator). The firm has operated for more than 25 years, offering advice across financial planning, mortgage planning, insurance, retirement planning, and saving and investing.

When the team came to ProfileTree, their existing digital presence did not reflect the depth of their expertise or the range of services they offered. Navigation was unclear, service content was underdeveloped, the branding needed refinement, and the site had no interactive tools to support client engagement. The brief was to build a new WordPress site that presented the firm professionally, ranked for relevant Irish financial services search terms, and gave visitors a reason to get in touch.

What We Did: The Web Design Approach

Brand Refinement and Visual Identity

We began with a brand review. The Financial Planner.ie identity was solid, but the logo and brand assets needed refinement to look consistent and professional across a modern website. We made targeted adjustments — nothing wholesale, but enough to give the digital presence a cleaner, more authoritative feel that matched the firm’s 25-year track record.

WordPress Build and Platform Choice

We built the new site on WordPress. For a financial advisory firm, the ability to update content without developer involvement is not optional — it is a practical necessity. Compliance requirements change. Products get updated. Staff move on and new team members need to be added. WordPress gives the Financial Planner.ie team the flexibility to manage all of this themselves, with a platform they can use without technical training.

SEO and Service Page Architecture

The previous site treated financial services as a list. We restructured the entire content architecture around dedicated service pages: Financial Planning, Mortgage Planning, Insurance (with sub-pages for Life, Income, and Business Insurance), Retirement Planning, Business Advice, and Saving and Investing. Each page was built around the specific search queries an Irish client would use when looking for that service.

Our keyword research focused on high-value terms within the Irish financial services market. Every service page was written to be keyword-rich without sacrificing readability or the credibility that regulated financial advice content requires. We worked closely with the Financial Planner.ie team throughout the content process to ensure every page accurately reflected their expertise and complied with their standards.

Interactive Financial Calculators

One of the core briefs was the inclusion of financial calculators embedded across the relevant service pages. These tools allow visitors to model savings, estimate costs, and explore investment options before speaking to an advisor — which both increases engagement time on the site and positions Financial Planner.ie as a firm that gives value before asking for anything in return. Calculators were integrated on the Financial Planning, Mortgage Planning, and Saving and Investing pages.

Navigation and User Experience

We restructured the navigation entirely around client intent. The primary menu reflects what a user is likely to be looking for — not how the firm internally organises its services. Clear calls to action were placed across every service page, and the mobile experience was built to match the desktop version in both functionality and clarity. A significant proportion of financial services searches happen on mobile, and the site needed to perform equally well on both.

Results

The new site delivered improved search visibility for industry-specific terms in the Irish financial services market, with targeted service pages now positioned to rank for the queries that bring qualified clients. Navigation clarity has improved significantly — visitors can move between service areas, calculators, and contact routes without friction.

The interactive calculators have created natural engagement points that did not exist on the previous site, giving visitors a reason to spend time with the content before making an enquiry. The WordPress build means the Financial Planner.ie team can now update content, manage their blog, and keep service information current without requiring external development support — which directly supports the ongoing search performance of the site.

How ProfileTree Approaches Web Design for Financial Advisors

Every financial services website project we take on starts with the same two questions: what does this firm want their website to do, and what is currently stopping it from doing that? For most financial advisors, the answers follow a familiar pattern. The site is not structured for service-level search queries. It cannot be updated without developer involvement. And it does not give potential clients enough of a reason to make contact before they are fully ready to commit.

Our approach for financial advisory businesses focuses on three things. A technical and content foundation that search engines can read and rank. A service architecture that puts individual services in front of the right search queries. And a user experience that builds trust fast — because in financial services, trust is what converts a visitor into an enquiry.

We build on WordPress because it gives financial services firms genuine control over their own digital presence. Regulatory changes, new products, updated team profiles, seasonal advice content — all of this can be managed internally, which means the site stays fresh and the firm stays in control.

If your financial advisory firm in Ireland or Northern Ireland needs a website that reflects your expertise and generates qualified enquiries, our web design services for professional services firms cover the full process from strategy and build through to SEO and content.

Frequently Asked Questions

What should a financial advisor website include to build client trust?

Trust signals matter more in financial services than in almost any other sector. At minimum, a financial advisor website needs clearly structured service pages that explain what the firm does and who it helps, a visible team section with credentials and photographs, client testimonials or case studies where regulations allow, regulatory accreditation details, and a contact structure that is easy to use. Interactive tools like calculators add practical value and demonstrate expertise before a client has even made contact. Plain language throughout is essential — financial advice is complex enough without the website adding to it.

How long does it take for a financial advisor website to rank in Irish search results?

For most financial advisory website projects, meaningful improvements in local and service-level search rankings appear within three to six months of launch, provided the site has been built with SEO from the ground up. More competitive terms — mortgage advisor Ireland, financial planner Dublin — take longer, sometimes six to twelve months, and require ongoing content work. The key variable is consistency: a site that adds new content, updates service pages, and maintains technical health will outperform a static site within the first year.

Do financial advisors in Ireland need separate pages for each service?

Yes. A single page listing financial planning, mortgage advice, retirement planning, and business insurance cannot rank competitively for any of those terms on its own. Each service has distinct search queries, distinct user intent, and distinct content requirements. Building dedicated service pages for each area is how a financial advisor website builds the topical authority needed to appear in search results when Irish clients are actively looking for specific advice. It also gives the firm the space to explain what each service involves in enough depth to be genuinely useful.

Can a financial advisory firm manage their own website after it is built?

Yes, if it is built on the right platform with the right setup. We build financial advisory websites on WordPress with a modular content system that allows the team to update service pages, add blog content, manage team profiles, and publish news or regulatory updates without any technical knowledge. For financial services firms operating under FCA or CBI requirements, the ability to update compliance-sensitive information quickly — without relying on a developer — is a practical necessity, not just a convenience.

What makes a financial advisor website different from other professional services sites?

Compliance requirements shape financial services websites in ways that do not apply to most other industries. Content must be accurate, not misleading, and in many cases must include specific regulatory disclaimers. Risk warnings may be required. The firm’s authorisation status needs to be clearly displayed. Beyond compliance, the trust threshold is higher: a client sharing detailed financial information with a firm needs to feel confident in that firm’s credibility long before picking up the phone. The design, content, and structure of the site all contribute to that first impression.

How much does a financial advisor website cost in Ireland?

Project costs depend on the size of the site, the number of service and sub-service pages required, whether calculator tools or other interactive features are needed, and the level of ongoing support included. We provide transparent scoping and pricing before any work begins. Contact us with details of your firm, your services, and what you need the website to achieve, and we will give you a specific quote based on your requirements.

ProfileTree is a Belfast-based website design and digital marketing agency that has worked with arts and community organisations across Northern Ireland and Ireland. This case study covers a full custom WordPress build for Féile...

First established in 2010 by seven local LGBT helplines, LGBT Ireland has grown into Ireland’s largest support service for lesbian, gay, bisexual and transgender people, as well as their families and allies. As part...

ProfileTree is a Belfast-based web design and digital marketing agency working with businesses across Ireland and the UK. This guide draws on our experience designing and developing digital platforms for tourism and leisure businesses,...