Investment portfolios, risk, return, assets and liabilities. We often hear these terms when any financial topic comes under debate. But what does any of that mean? What is an investment portfolio?

Before delving deeper into any financial terminology, we must first understand investment.

Why do people invest, and how do they go about it? Simply put, investing is spending resources in return for expected future profits. Even more simply put, investment is making your money “work for you”.

A more technical definition would refer to investment as a commitment of resources for some time to derive future profits that would compensate for the initial spending of money and time, the risk investors take and the rate of expected inflation.

There are many ways to invest and even more types of investments. People nowadays invest in stock, real estate, bonds, cryptocurrency, and other financial products.

The upfront money given as capital, investment or seed money is perceived as a loan. Investors will only put their resources on the line if the generated income or return is worthwhile.

The profits generated from initial investments are often called ROI or return on investment. These returns take the form of stock dividends, coupons in bonds or interest in loans.

Return, however, is not the only thing to consider when making investments. The volatility or the perceived level of risk involved in each investment opportunity ultimately decides the attractiveness of any financial venture.

People usually invest for one simple reason: foregoing a percentage of their consumption today for bigger profits. Tomorrow guarantees the flow of money continuously if done right.

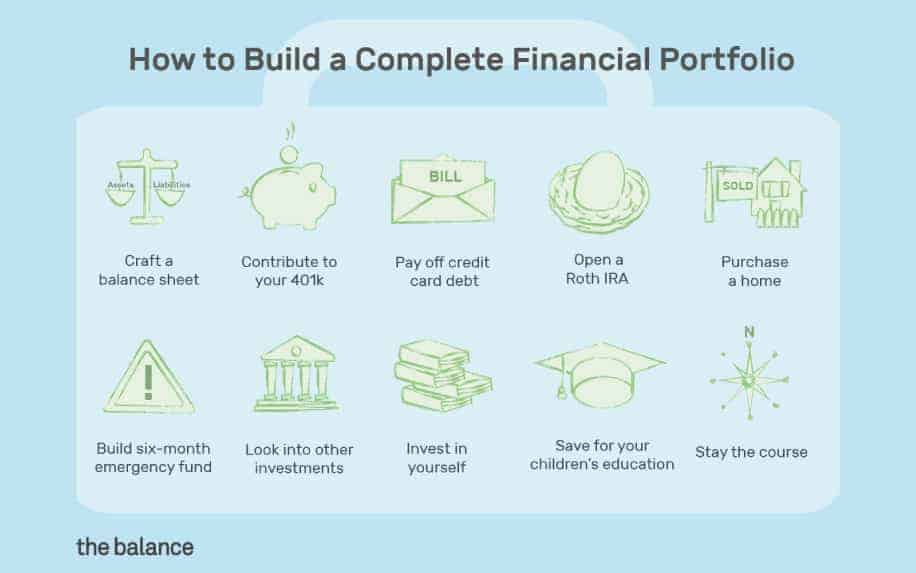

The perfect financial portfolio can comprise several different elements. Image credit: TheBalance

The Nature of Investment Portfolios

The nature of the market worldwide mostly depends on free cash flow activities, meaning that money always circulates in the market. A viable investment has a good return relative to the initial investment and its perceived risk.

There are many ways to invest and many types of different investments that can be included in your portfolio.

Ownership Investments

Ownership investments typically include buying undervalued assets while selling overvalued ones. In other words, buy cheap and sell high. Investors can own stocks, real estate or even whole businesses.

The investor then chooses to sell their holdings later for a price higher than initially paid, generating revenue.

Lending Activities

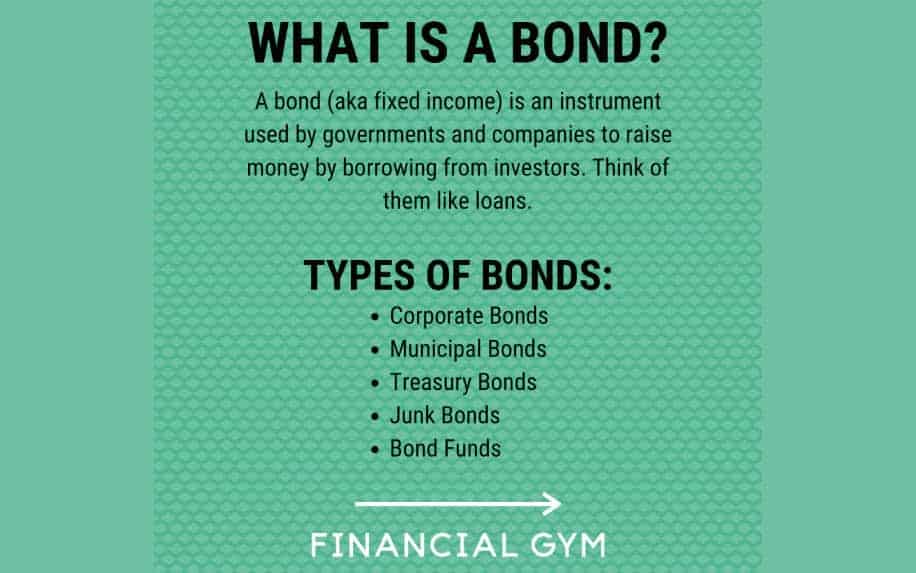

A bond is a loan to a company that will be paid back to the bondholder with interest.

Companies issue bonds to borrow money at an interest rate less than a bank’s while rewarding the bondholder with interest more than they would typically get from interest generated from bank saving accounts.

Aside from bonds, other lending activities include options, government or federal certificates and your typical bank savings account.

Bonds are a popular low-risk investment product. Image credit: Pinimg

Alternative Investments

Other unclassified types of investment which do not fall under the 2 categories listed above would include investing in foreign currency exchange (FOREX), Debt purchasing or taking advantage of short-term price fluctuations such as those seen in gold.

These strategies have a very short investment horizon, often called day trading.

However, these alternative investment methods are better off left to the pros. This is because they require experience a deeper knowledge of the finance mechanism, and more familiarity with global micro and macroeconomics.

Investment Portfolios: Scratching the Surface

Getting to the real investment portfolio definition is not simple. It means something different for everyone. The term “portfolio” is thrown around in many different workplaces.

A writer has a portfolio of his/her writings. Artists have portfolios that include paintings or drawings; even architects have design portfolios with earlier work and sketches. However, an investor’s portfolio is something entirely different.

A financial portfolio is the sum of your assets, investments, and liabilities.

An investor’s portfolio would look like the pizza you would order on a lazy Sunday afternoon. It’s divided into slices, each representing a portion of the investor’s financial holdings.

These holdings can be large-cap growth stocks, high-yield bonds, cash equivalents or assets.

The portfolio as a whole is given a certain risk and return rating. The risk given to a complete portfolio is calculated by factoring in the risk of each investment inside the portfolio.

Your average investor would likely try to keep the return as high as possible while retaining a low-risk rating. Most investors are risk-averse, meaning they prefer to avoid or lower risk as much as possible, even if it means decreasing the expected return. Potential investments for risk-averse investors may include low-risk government bonds, certificates of deposit, or index funds, while an investor lists may include individuals who have a low tolerance for risk and prioritize preserving their capital over making high returns.

After making the portfolio definition clear, we must mention the famous economist “Harry M. Markowitz,” who provided a theory called “The Modern Portfolio Theory” (MPT for short).

This theory bases a few assumptions on how investors structure their portfolios.

The two main concepts of the modern portfolio theory are that most investors will do what they can to maximise return while minimising risk. The second concept is that risk can be minimised by utilising a well-diversified portfolio.

Statistics and data points I could add to support portfolio construction and diversification:

A portfolio with diversification across asset classes sees about 20% less volatility on average vs. a single asset portfolio (Vanguard research).

Adding international stocks to a portfolio can lower total volatility by 3 percentage points or more (Fidelity).

During market downturns, a globally diversified portfolio suffers smaller maximum drawdowns. In 2008, diversification reduced max drawdown from -47% to -26% (DALBAR analysis).

According to Morningstar, a diversified portfolio aligned to an investor’s risk tolerance and goals achieves an average annual return of 1-2% higher.

Portfolios optimized using Modern Portfolio Theory can achieve the same expected return with 15-20% less risk (Journal of Financial Planning).

Academic studies show that strategic rebalancing can boost cumulative returns by 0.4% annually while lowering volatility (Vanguard, Morningstar).

Investors using automated rebalancing strategies saw returns increase 0.30% annually compared to no rebalancing (Betterment research).

Diversify? Why Not Just Pick a Winner?

Now that the portfolio definition is clear, we can discuss portfolio diversification. You might have heard of “diversification” before, but what exactly is portfolio diversification?

Reducing risk while retaining the same level of return? Ludicrous, you might say. High return equals high risk.

Not necessarily. A well-diversified portfolio could reduce risk rating while retaining or maximizing returns.

Diversifying your investment portfolio helps to shield you against risk. Image credit: RamseySolutions

Think of it like this: you have twelve eggs and must transport them from point A to point B. Sure, you can pile them all in the same basket. Along comes a friend with an extra basket. You think to yourself, maybe two light baskets would be easier than one heavy one.

On route, one of the baskets gets torn up, and you lose six eggs. It’s a loss, sure. But at least you didn’t lose all twelve. “Don’t put all your eggs In one basket” is a phrase that perfectly describes the need for portfolio diversification.

Any industry’s fate can be overturned overnight for many reasons—shortage of supplies, decreased price of alternatives, governmental restrictions or even political forces.

For example, a group of people decide to diversify their portfolio; they use their investment to buy stocks in five different automotive companies. When one of those companies falls short, the others are bound to rise.

This type of diversification makes the portfolio holder somehow protected. However, let’s say that economic conditions lead to fuel costs going dramatically up. Suddenly, driving seems too expensive.

A well-diversified portfolio will include investments that are not correlated, meaning that each investment inside the portfolio is either inversely or disproportional to one another.

So if one goes down in value, the others will balance out this loss.

Investing in different companies, diverse industries, and even countries is the best way to have a well-diversified portfolio. Diversification, however, does not eliminate risk; it only reduces it.

The Road To Building Your First Portfolio

Most investors are risk-averse, meaning they prefer to reduce risk even if the return is minimised. However, no two portfolios are the same. How do you allocate your resources?

Do you go for high-risk/high return? Do you play it safe and settle for less profit? Building a portfolio can be daunting, given the many variables in play. The first and most important step is to understand why you want to invest in the first place.

Are you saving for a long-term goal? Are you willing to take risks? If so, how much risk is too much? All these are questions you should ask yourself before engaging in investment activities.

From afar, building a portfolio sounds simple; just buy different stocks, invest in startup businesses, own some assets or play it safe and buy low-return bonds. In truth, there is much more to it.

How to solve this dilemma? Here are some steps to follow for beginner investors.

Find Your Purpose

No matter why you’re investing, there’s a suitable portfolio for you. It all depends on what you want to do with your profits. If you’re saving up for a long-term goal, there are low-yield bonds, which offer a low level of risk.

As mentioned earlier, most investors are risk-averse. What about those who venture into the riskier investments, though? First, you must understand that investment is not gambling, even with high-risk assets.

Higher risk indeed provides a higher return if the investment is successful. The investor must be paid a premium for the risk they take. Knowing the purpose behind your investment needs is the first key to opening your portfolio door.

Assess your Risk Tolerance

How much risk are you willing to take? Reverting to the first key. With high risk and volatility, losing a chunk of money is possible.

However, with a well-diversified portfolio, that loss can be mitigated. Assessing your risk tolerance is important in determining where to allocate your resources. Do you go for safe, low-yield municipal bonds and certificates of deposit?

Or do you risk high and allocate your resources to IPOs (initial public offerings) and high-yield, long-term bonds?

Different financial products carry different levels of risk. Image credit: SlideTeam

Study the Market

When it comes to designing an investment portfolio, you have countless options. Publicly traded companies are everywhere. Everyone is issuing stocks. What to buy, what to avoid? How volatile is the investment you’re considering? Is it in constant rise and decline?

Investors don’t just throw their money at flashy-looking stocks or new “fad” bonds. They study the market. Companies are never stable; what goes up must come down. Study the company’s performance you are considering investing in, and read past financial data.

Is the company heavily reliant on equity financing? Does it have too much debt? Are there any signs of collapse? Thoroughly check up on prospective investments before barging in. As stated before, investment is not gambling.

Have a Plan

What is your endgame? All investors have a plan that returns to the first key: Find your purpose. Your investment plan should be clear and precise. Do you use your profits to invest more?

Or do you save your winnings for a later time? Although your plan can change, you must stick to your ultimate goal. Find your end game and plan accordingly how to get there.

Allocate your Resources

You found your purpose, assessed how much risk you’ll be willing to take, studied the market and devised a brilliant plan. Now comes the fun part: allocate your resources.

Find how much disposable income you have set aside and make that money work for you. Following the previous steps, you should know exactly where you want to put your money and what you want to invest in.

Diversify your Investment Portfolio

Do not put all your eggs in one basket. Consider different asset types, buy stocks from different companies in different sectors, put some money in low-risk assets or even think about buying stocks from foreign companies.

Diversification is vital; it helps mitigate any potential losses. If you lose money on one of your investments, you have others to help ease the pain.

Measuring Investment Portfolio Performance

Set appropriate benchmarks based on goals, risk tolerance and asset allocation.

Calculate and track total return annualized returns over time horizons.

Evaluate risk-adjusted returns using Sharpe, Sortino and alpha ratios

Compare performance to benchmarks and market indexes

Use attribution analysis to understand drivers of return

Portfolio Rebalancing Strategies

Periodic rebalancing, like annually or quarterly

Threshold-based rebalancing when allocations skew by X%

Time-based rebalancing at specific intervals (every 6 months)

Rebalance selectively by asset class rather than the entire portfolio

Tax Considerations

Use retirement accounts to hold assets with higher turnover

Match losses to offset capital gains for tax efficiency

Harvest tax losses toward the end of the year if the portfolio permits

Hold assets providing dividends or income in tax-advantaged accounts

Avoiding Emotional Biases

Don’t panic sell during market declines based on fear

Avoid buying “hot” assets simply due to strong momentum

Rebalance to stay true to target allocations, ignore short-term swings

Have predetermined sell disciplines for pruning poor performers

There are also some warning signs to indicate a crash or collapse of a stock, currency or company. Keep up to date with the latest business information and financial updates. It is never too late to enter the investment game.

Whether you need money a year or ten years from now, there is much more you can do with your money other than settling for the measly interest a regular bank savings account provides you.

Lucrative business opportunities are always around the corner. Invest right, play it smart, and always research before entering new investment opportunities.

As mentioned earlier, investment is not a gamble.

You will likely come on top with the right information, meticulous research, and smart resource allocation. There is always a possibility of loss in the financial market. That’s why you should only use your disposable income for investment.

Risk is a factor that should always be considered when putting your money to work. You might have the stomach to take on a high-risk/high-reward investment, but always consider the worst-case scenario and do your best to hedge your losses.

The importance of diversification in any investment portfolio is unfathomable. Learn more along the way. A smart investor will learn from past losses and be alert for new information and opportunities.

The use of a financial advisor at first is a smart idea. Not only will you learn the basics and pick up many tips, but a financial advisor is someone with years of experience who is unlikely to steer you wrong.

However, those who wish to venture into the financial market start slow, learn from mistakes, study the market and learn how to read a company’s financial sheets.

It might seem like a terrifying experience, but with the right tools, knowledge and proper funding, any average Joe can start immediately on his portfolio and investment opportunities.

Investment Portfolio FAQ

Q: How often should a portfolio be rebalanced?

A: Most experts recommend rebalancing at least annually or when allocations skew 5-10% from targets.

Q: What asset allocation is best for a portfolio?

A: The optimal allocation depends on your risk tolerance and goals. A good starting point is 60% stocks and 40% bonds.

Q: How many stocks should be in a portfolio?

A: Research suggests 12-20 stocks provide adequate diversification. Much more brings diminishing returns.

Q: What portion of a portfolio should be international?

A: Having 20-40% international stocks and bonds helps reduce volatility through diversification.

Q: How important is keeping fees and taxes low?

A: Minimizing costs and taxes can improve net returns over the long run.

Investment Portfolio Conclusion:

Constructing a robust investment portfolio requires aligning with your risk appetite, return requirements, and time horizon. Apply core principles like asset allocation, diversification, and rebalancing. Measure performance rigorously and course-correct when needed. Avoid emotional decision traps.

Continually optimize your portfolio by following the data-driven best practices outlined in this guide. With discipline and the right strategic approach, your investments can generate optimal returns to meet your financial life goals.

Product management is an exhilarating journey filled with innovation, collaboration, and the pursuit of creating products that meet market needs. On the one hand, product managers...

In a digital age where time is as valuable as currency, small and medium-sized enterprises (SMEs) are increasingly turning to automation to enhance productivity and stay...