Digital Marketing for Finance Audiences: UK and Ireland Guide

Table of Contents

For finance audiences and independent financial advisers, referrals remain the backbone of practice growth. Referrals are valuable, but they have a ceiling. The client who found your name through a friend still Googles you before they call. Your website, your reviews, and the content you publish are all being assessed before that first conversation ever happens.

For financial advisers across the UK and Ireland, digital marketing is no longer a nice-to-have. It is the first impression your practice makes on every prospective client who finds you through a search. This guide covers the strategies that work for IFAs operating in a regulated environment: local SEO, FCA-compliant content marketing, social proof, video, and how to measure what is actually driving enquiries.

Why Digital Marketing Now Matters for Finance Audiences and IFAs

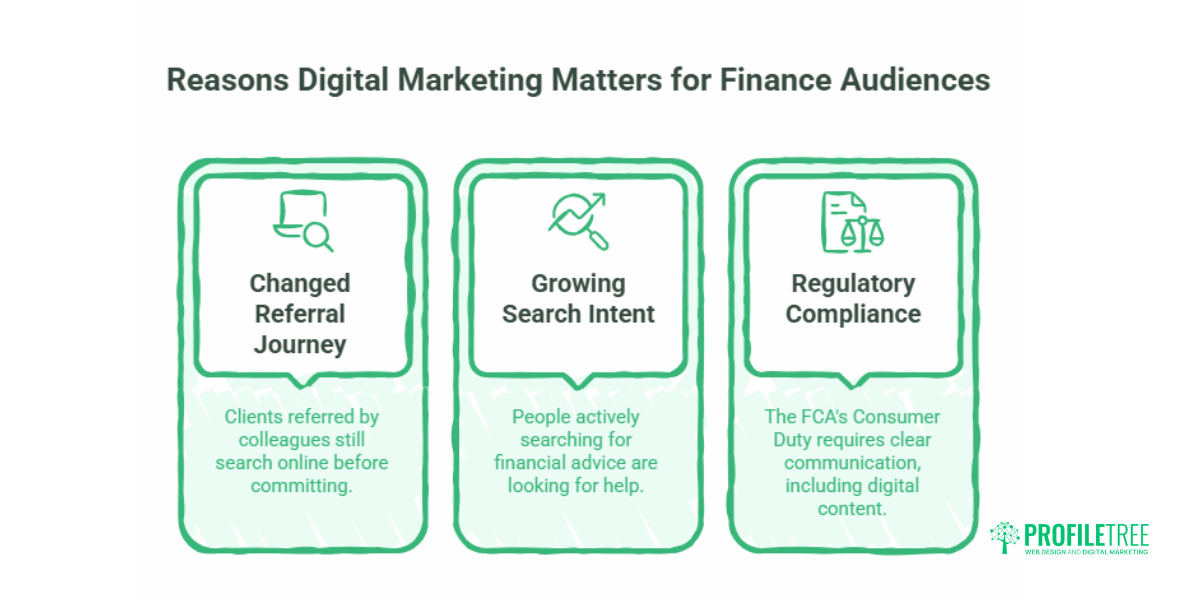

The way prospective clients find financial advisers has changed. Search engines are now part of the referral journey, not separate from it. A client referred by a colleague will still search your name, read your reviews on Google or VouchedFor, and browse your website before committing to a call. If any of those touchpoints raise doubt, the referral goes cold.

Beyond referrals, search intent for financial advice is growing. Queries like “financial adviser Belfast,” “IFA near me,” and “independent financial adviser [city]” represent people who are actively looking for help, not passively browsing. These are high-intent searches from prospective clients at the exact moment they are ready to take action. The IFAs who appear in those results consistently win those clients. Those who do not are invisible to a significant share of the market, regardless of how good their advice actually is.

There is also a regulatory dimension. The FCA’s Consumer Duty, introduced in 2023 and now embedded in ongoing supervision, includes a specific “Consumer Understanding” outcome. That outcome requires firms to communicate in a way that consumers can understand, test whether communications support good outcomes, and act where they do not. Digital content, including your website, blog posts, and social media activity, falls within scope. Getting digital marketing right is no longer just a growth decision; for regulated firms, it is part of meeting your obligations.

Pillar 1: Your Website as a Trust Architecture

For a financial adviser, the website is not a brochure. It is the first compliance document most prospective clients will read, and the primary trust signal before any conversation takes place.

Speed, Mobile Experience, and First Impressions

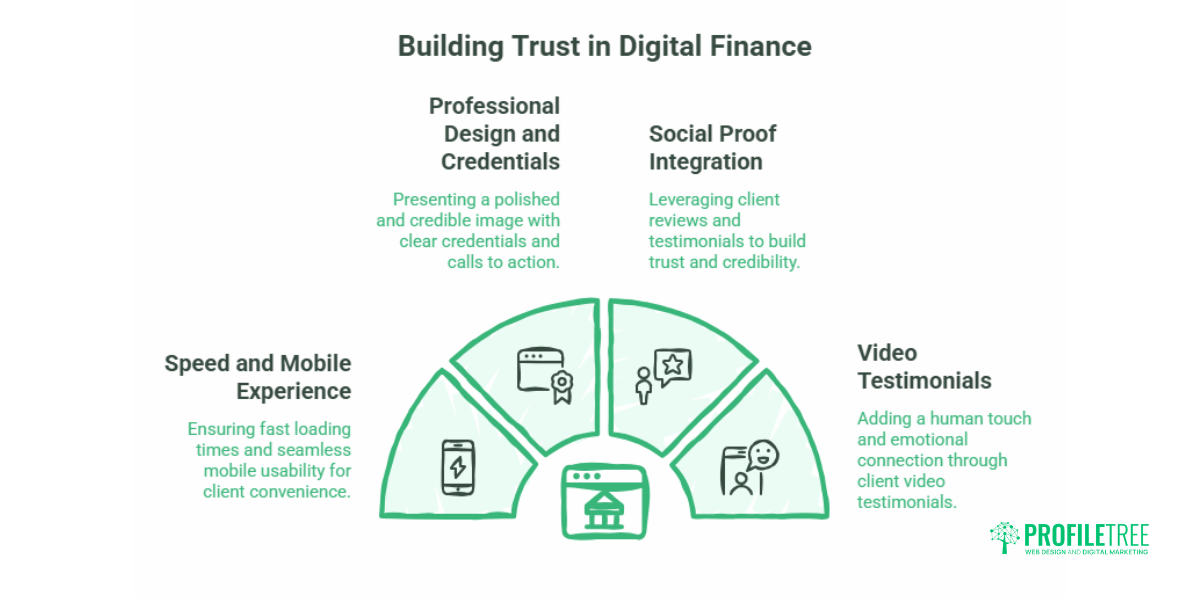

High-net-worth clients and business owners researching financial advice are often searching on mobile devices during commutes or between meetings. A website that loads slowly or fails to display cleanly on a phone creates an immediate credibility problem. Google’s Core Web Vitals now directly influence search rankings, so a slow site loses visibility as well as conversions.

A professional website for a financial adviser should load in under three seconds on mobile, present credentials clearly above the fold, and make the call to action (whether that is a phone number, a booking link, or a contact form) visible without scrolling. ProfileTree’s web design work with professional services firms focuses on exactly these priorities: structure that earns trust before the visitor reads a word of copy.

Integrating Social Proof into the Site Architecture

In the UK, VouchedFor and Google Reviews are the two platforms that matter most for financial advisers. VouchedFor specifically is used by prospective clients who are actively comparing advisers, and a strong rating there converts browsers into enquiries at a measurably higher rate than generic testimonials on your own site.

Your website should surface these reviews prominently, link to your VouchedFor profile, and display your Google rating with a review count. A dedicated testimonials page is useful, but embedding recent reviews on the homepage and service pages is more effective. Client video testimonials, where clients have consented, and FCA financial promotion rules are observed, add a human dimension that text cannot replicate.

Pillar 2: Local SEO: Winning the “Adviser Near Me” Search

Most financial advisers serve a defined geographic area. Even those who operate nationally often win the majority of their clients from their home city or region. Local SEO is the discipline that makes your practice visible when someone in your area searches for financial advice.

Google Business Profile

Your Google Business Profile is the single most important local SEO asset you control. An optimised profile will appear in the map pack (the three-result box that appears at the top of Google results for local searches) for relevant queries in your area. To achieve this, your profile needs to be fully completed, your practice address and phone number must be consistent with what appears on your website, your service categories must be accurate, and you must actively collect and respond to Google reviews.

A standard Google Business Profile checklist for IFAs:

- Business name matches your FCA register entry exactly

- Primary category set to “Financial Planner” or “Financial Adviser” as appropriate

- Services section completed with specific offerings (pension advice, inheritance tax planning, mortgage advice)

- Opening hours are accurate and updated for bank holidays

- At least 10 recent Google reviews with responses from the practice

- Posts updated at least monthly with educational content

- Photos include the office exterior, interior, and the adviser (builds local recognition)

On-Page Local Signals

Beyond your Google Business Profile, your website needs to reflect your location clearly. Your homepage should mention the city or region you serve within the first paragraph. If you serve multiple locations, separate location pages with genuinely distinct content that performs better than a single page with a list of towns.

For practices in Northern Ireland, the dual-jurisdiction question (whether a client’s query falls under UK FCA regulation or Central Bank of Ireland oversight) is a genuine differentiator. Addressing this clearly on your website answers a question that many prospective cross-border clients have, but few advisers answer in their content.

ProfileTree’s work on digital marketing in Northern Ireland covers the specific challenges of operating in a dual-market context, which is particularly relevant for advisers serving communities across the border.

Pillar 3: Content Marketing Under Consumer Duty

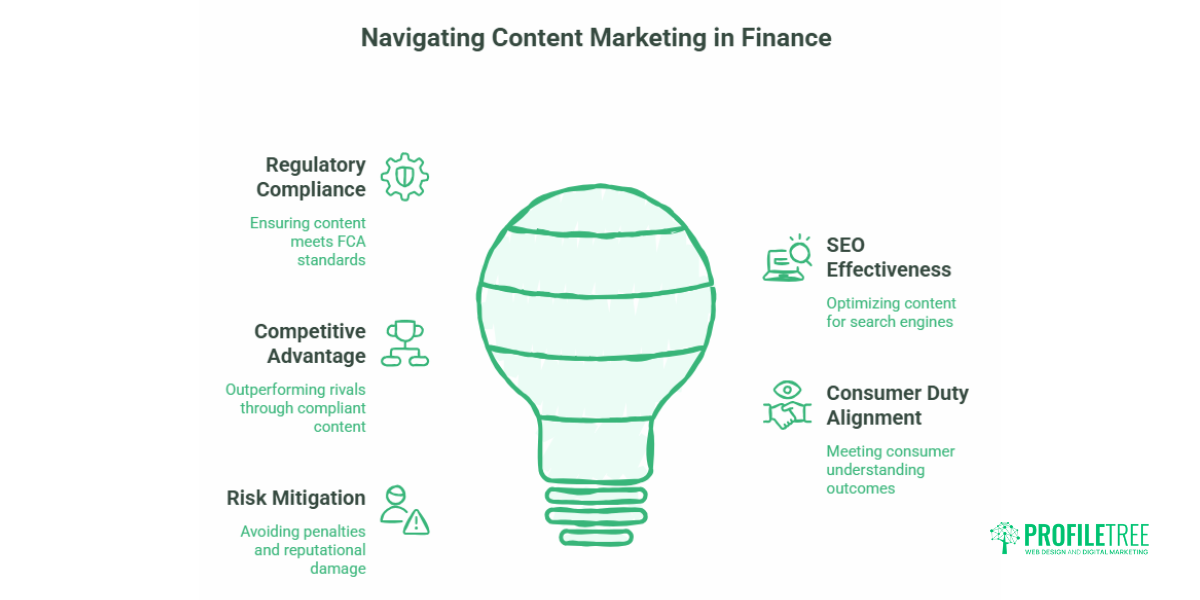

Content marketing for financial advisers is complicated by regulation, but regulation also creates opportunity. Most generic marketing guides (particularly those written for US audiences) ignore the FCA entirely. In the UK, the adviser who understands how to create content that is both SEO-effective and FCA-compliant has a significant advantage over competitors who either avoid content marketing altogether or produce it without proper oversight.

The Consumer Duty “Consumer Understanding” Outcome

Under Consumer Duty, firms must ensure that communications support good outcomes for retail customers. In practice, this means marketing content should avoid jargon that obscures meaning, should not overstate potential benefits or understate risks, and should be tested periodically to confirm it is working as intended.

For content marketing purposes, this translates into a clear editorial framework: write to inform, not to sell. Educational blog posts explaining how pension annual allowances work, what to consider when approaching retirement, or how to assess protection needs are valuable to the reader, serve a genuine informational purpose, and are unlikely to trigger financial promotion rules because they are not promoting a specific product or arrangement. Content that crosses into product promotion (recommending specific funds, quoting projected returns, or directing readers toward particular financial arrangements) requires compliance sign-off before publication and appropriate risk warnings.

What to Write About

The content topics that perform well in search for IFAs are consistently aligned with the questions clients ask before and during the advice process:

- How much should I have saved by retirement at [age]?

- What happens to my pension when I die?

- Should I consolidate my pension pots?

- What is the difference between a financial adviser and a financial planner?

- How do I find a good IFA near me?

- ISA vs pension: which is better for me?

Each of these questions represents a real search query with real prospective clients behind it. A financial adviser practice that publishes a clear, jargon-free answer to each question builds a content library that attracts organic search traffic, demonstrates expertise, and pre-qualifies prospective clients before they make contact.

ProfileTree’s content marketing services for professional services firms focus on building this kind of evergreen content infrastructure rather than chasing short-term trends. The digital marketing compliance in financial services article on our site covers the regulatory framework in more detail for firms that want to build their own internal processes.

The Compliance Sign-Off Workflow

For any content that could be construed as a financial promotion (which includes blog posts that reference specific products, social media posts referencing investment performance, and email newsletters discussing particular strategies), FCA-regulated firms need a sign-off process. A simple workflow involves the content being drafted, reviewed by an appointed compliance officer or nominated reviewer, approved or returned with amendments, and then archived with a date stamp for the required retention period.

Building this workflow before you scale content production saves significant remediation work later. It also means your compliance officer has sight of what is being published, which protects the firm.

Pillar 4: LinkedIn and Social Media Within Compliance Guardrails

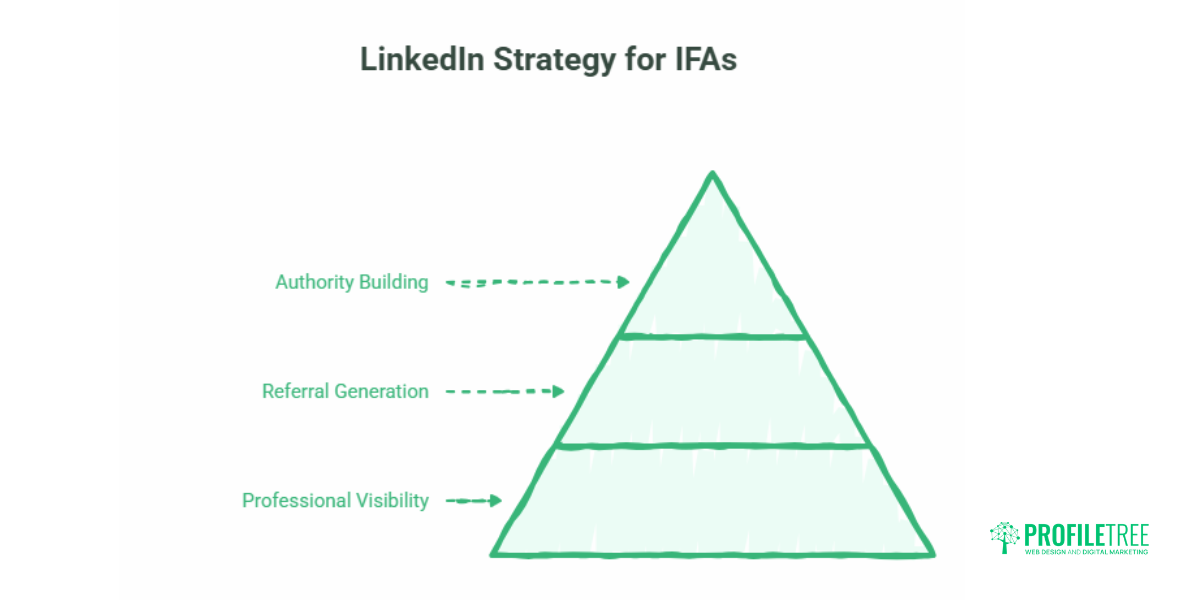

LinkedIn is the primary social platform for IFAs building professional visibility. It serves two distinct purposes: generating referrals from professional contacts such as accountants and solicitors, and building authority with prospective clients who are assessing you before making contact.

The Authority Strategy for LinkedIn

Posting consistently on LinkedIn about the questions your clients ask, the misconceptions you encounter most frequently, and the changes in regulation that affect your clients’ planning positions you as a knowledgeable and accessible professional. Posts do not need to be long. A short observation about a common pension planning mistake, a clarification of how the annual allowance works after a Budget change, or a reflection on a genuine planning challenge (appropriately anonymised) will consistently outperform promotional announcements.

The guardrails matter. Anything that could be read as a recommendation, a projected return, or a specific product suggestion requires the same compliance treatment as a formal financial promotion. The safest approach is to stick to educational and informational content on social media, reserving any product-specific communication for regulated channels.

Social Proof on Social Media

Sharing client reviews from VouchedFor or Google (where the client has given explicit consent) is one of the most effective uses of social media for IFAs. A genuine review from a real client, shared with their permission, is more persuasive than any amount of promotional copy. Soliciting reviews systematically after every completed piece of work, rather than ad hoc, builds the volume needed to make this a reliable content source.

The ProfileTree guide to social media content strategy covers the structural approach to building a consistent social media presence for professional services firms.

Pillar 5: Paid Media and Lead Generation Platforms

Organic search and content take time to build. For practices that need to generate enquiries in the shorter term, or that want to supplement organic growth, paid channels offer a more immediate route to visibility.

Google Ads vs Lead Generation Platforms

The two primary options for IFAs in the UK are Google Ads (pay-per-click search advertising) and paid listing platforms such as Unbiased and VouchedFor. These serve different purposes and carry different risk profiles.

| Channel | Typical cost per lead | Intent level | Compliance risk | Long-term ROI |

|---|---|---|---|---|

| Google Ads | Medium to high | High | Medium (ad copy requires approval) | Good if managed well |

| Unbiased | Per-lead pricing | Medium to high | Low (platform manages) | Good for volume |

| VouchedFor | Subscription plus leads | High | Low (platform manages) | Strong for conversion |

| Organic SEO | Time investment upfront | High | Low | Excellent long-term |

Unbiased tends to generate more leads by volume; VouchedFor tends to generate fewer but higher-converting enquiries because the review system builds credibility before the client makes contact. Neither replaces a strong organic presence, but both can work as part of a balanced lead generation approach.

Budget Benchmarks

As a starting point, practices focused on growth typically allocate between 5% and 10% of gross revenue to marketing, with the balance between paid and organic depending on how established the practice is. A newer practice with limited organic authority may front-load paid spend while building content. A more established practice with strong Google rankings and VouchedFor reviews may reduce paid spend over time as organic enquiries increase.

Video for Financial Advisers: Building the Human Connection

Financial advice is a relationship business. Clients are trusting an adviser with decisions that will affect their financial security for decades. Before they commit to that relationship, they want to feel they know and trust the person they are dealing with.

Video is the most direct way to create that human connection at scale. A short introductory video on your website’s homepage, filmed professionally and simply, does more to build pre-consultation trust than almost any other single investment in your digital presence. It lets prospective clients see how you communicate, gauge your approachability, and decide whether you are the right fit before they spend time on either side in an introductory call.

For financial advisers, the compliance considerations for video are similar to those for written content. An introductory video that explains your approach, your qualifications, and the kinds of clients you help is unlikely to constitute a financial promotion. A video that discusses specific investment strategies, projected returns, or particular products needs the same sign-off as any other financial promotion.

ProfileTree’s video production work with professional services firms includes compliance-aware briefing as standard, so the finished content meets both the creative and regulatory requirements.

Measuring What Is Actually Working

The most common digital marketing mistake financial advisers make is investing in activity without measuring outcomes. Understanding which channels are generating enquiries (not just website visits) is what allows you to allocate budget intelligently and stop spending on what is not working.

The measurement framework for an IFA practice should track:

- Organic search traffic: how many visits are coming from Google each month, and which pages are driving them

- Local search visibility: how often your Google Business Profile appears in searches, and how many calls and directions requests it generates

- Enquiry source attribution: where clients say they found you, and whether that matches your analytics data

- Review growth: the rate at which new reviews are being added to VouchedFor and Google

- Content performance: which blog posts are attracting the most search traffic and generating the most time on page

Google Analytics 4 and Google Search Console, both free, provide the core data for organic performance. Your Google Business Profile dashboard provides local visibility data. Asking new clients how they found you (and recording the answer) provides the qualitative layer that analytics alone cannot capture.

ProfileTree’s email marketing compliance for finance article covers the data and attribution considerations specifically for email-driven campaigns within regulated practices.

Getting Started: A 90-Day Digital Roadmap

For an IFA practice with limited time and a clear need to improve digital visibility, the priority order matters. Attempting everything at once produces mediocre results across the board. A sequenced approach builds momentum.

Weeks 1 to 4: Audit your Google Business Profile and get it fully completed. Audit your website for speed, mobile experience, and clarity of credentials. Identify the three or four search queries you most want to rank for locally.

Weeks 5 to 8: Publish two or three educational blog posts addressing the questions your clients ask most often. Brief your compliance officer on the content sign-off process. Ensure your VouchedFor profile is complete, and begin systematically asking for reviews after client work.

Weeks 9 to 12: Review your LinkedIn activity and establish a consistent posting rhythm. Set up Google Search Console to track your organic performance. Assess whether a Google Ads campaign or an unbiased listing would complement your organic activity.

This is not a complete digital marketing programme; it is a foundation. The practices that build consistently on this foundation over 12 to 24 months (publishing regularly, collecting reviews, improving their website incrementally) are the ones that eventually dominate local search in their area.

FAQs

How do financial advisers get clients online?

The most effective route is combining local SEO (appearing in Google search results for “financial adviser [city]” queries) with a strong review presence on VouchedFor and Google. Content marketing (publishing educational blog posts that answer the questions prospective clients search for) supports both organic visibility and pre-consultation trust-building. Paid platforms like Unbiased can supplement organic enquiries, particularly for newer practices building their online presence.

Is LinkedIn worth it for IFAs?

Yes, for two distinct purposes. First, it builds referral relationships with accountants, solicitors, and other professionals who encounter clients needing financial advice. Second, it builds authority with prospective clients who are assessing advisers before making contact. Consistent, educational posting outperforms promotional content significantly. Compliance guardrails apply: financial promotions on LinkedIn require the same sign-off as any other regulated communication.

How much should a financial adviser spend on digital marketing?

Practices focused on growth typically allocate 5 to 10% of gross revenue to marketing activity. The balance between paid and organic channels depends on how established the practice is and how quickly results are needed. Organic SEO and content marketing have higher upfront time costs but deliver compounding returns; paid lead generation platforms provide faster but ongoing cost-per-lead expenditure.

Does the FCA regulate financial adviser websites?

Yes. A financial adviser’s website is considered a financial promotion under FCA rules (COBS 4) where it communicates an invitation or inducement to engage in investment activity. This means website content, blog posts, social media, and email marketing all fall within the financial promotions regime where they reference specific products, services, or investment outcomes. Educational content that does not constitute a promotion is outside the scope, but the distinction requires careful application. The FCA’s Consumer Duty also requires firms to ensure their communications support good consumer outcomes.

Which is better for IFAs: Unbiased or VouchedFor?

They serve different purposes. Unbiased generates more leads by volume through its consumer-facing platform. VouchedFor generates fewer but typically higher-converting enquiries because the review and rating system allows prospective clients to assess an adviser’s track record before making contact. Many practices use both alongside organic search rather than treating them as alternatives.

Can I use AI to write financial content for my website?

AI tools are useful for drafting and structuring content, but financial services content requires human expert review before publication. The primary reasons are accuracy (AI can produce plausible-sounding but incorrect information about tax rules, allowances, and regulatory requirements) and compliance, since any content that could constitute a financial promotion requires sign-off by an appropriate person within the firm, regardless of how it was drafted.

Conclusion

Digital marketing for financial advisers is not about chasing every new platform or producing content for its own sake. It is about being visible when prospective clients are looking, building credibility before the first conversation, and communicating in a way that meets both the FCA’s standards and the expectations of clients who now research everything online before making a decision.

For IFA practices across Northern Ireland, Ireland, and the UK, the combination of local SEO, FCA-compliant content, a strong review presence, and professional video is what consistently builds sustainable enquiry pipelines. If you want to discuss how ProfileTree can support your practice’s digital marketing, get in touch with our team.