Small Business Failure Rates: UK Data and How to Beat Them

Table of Contents

In the UK, the Office for National Statistics (ONS) business demography data consistently shows that around 20% of new businesses close within their first year. By year five, approximately 50% have ceased trading. These figures have remained broadly stable for over a decade, which tells you something important: the causes of small business failure are structural, not cyclical.

The survival picture improves significantly for businesses that pass the five-year mark. Businesses that have operated for more than five years have demonstrated they can adapt to changing conditions, manage cash flow through at least one difficult period, and retain customers beyond the initial launch phase. The steep drop-off happens in years one to three.

Northern Ireland’s business survival rates track closely with the UK average, though the economic context differs. The Northern Ireland economy has a higher proportion of micro-businesses (fewer than ten employees) than the UK as a whole, and these smaller operations face sharper cash flow pressures and more limited access to growth capital. That said, Northern Ireland also benefits from specific support structures, including Invest NI programmes and access to InterTradeIreland funding, that aren’t available to businesses elsewhere in the UK.

The statistics matter less than what drives them. Knowing that half of businesses fail within five years is sobering. Knowing why they fail is actionable.

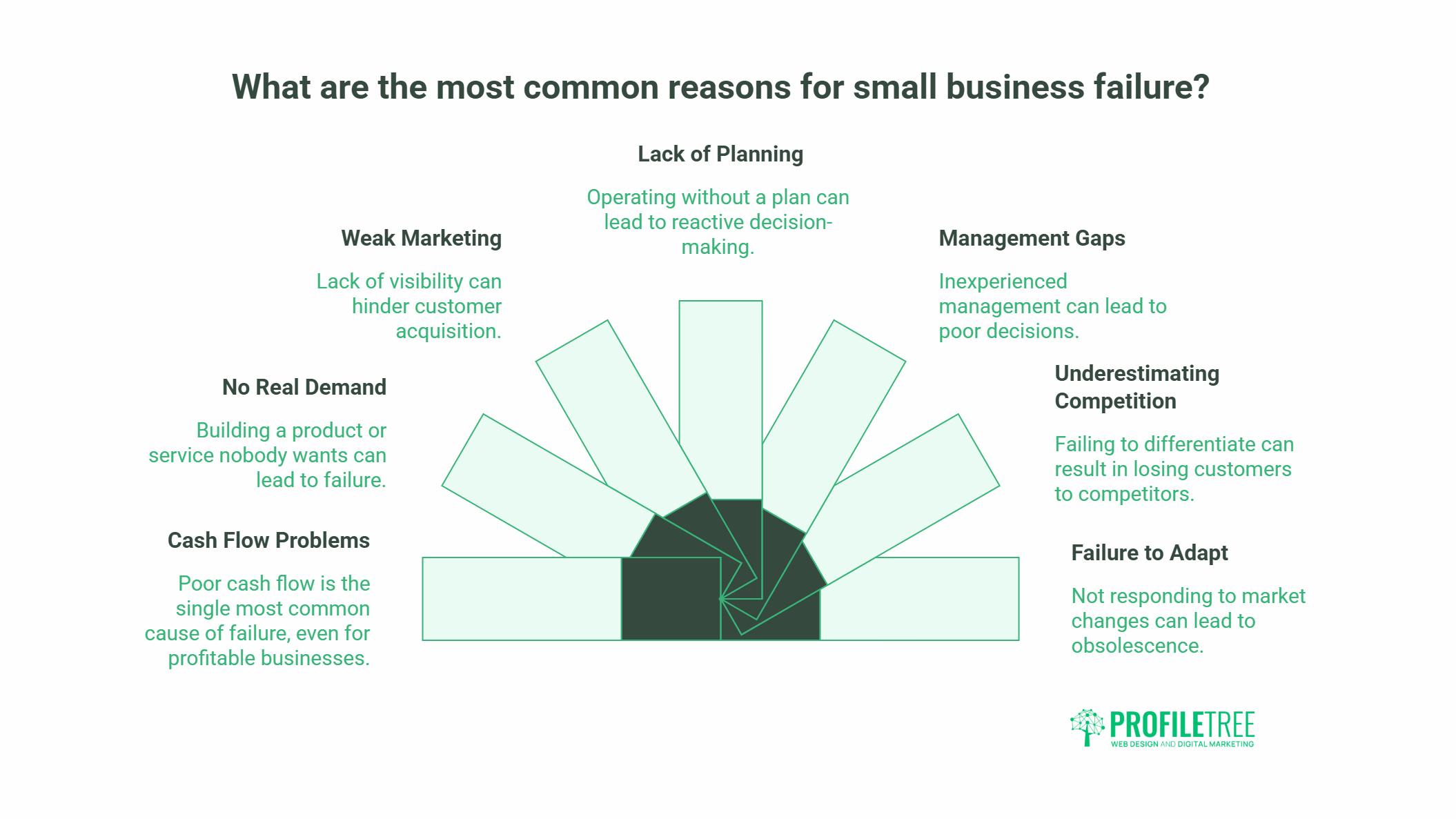

The Seven Most Common Reasons Small Businesses Fail

These causes aren’t equally weighted. Cash flow problems and lack of market demand account for the majority of failures. The others compound those two problems when they’re already present.

1. Cash Flow Problems

Poor cash flow is the single most common immediate cause of small business failure. A business can be profitable on paper and still run out of money if customers pay late, if seasonal income creates gaps, or if the owner draws more than the business can sustain. Many businesses that fail aren’t fundamentally unviable; they simply run out of cash before they can become self-sustaining.

The fix isn’t complicated, but it requires discipline: maintain a cash flow forecast updated at least monthly, build a cash buffer covering three months of operating costs before you need it, and address late payment from customers immediately rather than letting it accumulate.

2. No Real Demand for the Product or Service

The second most common cause is building something nobody wants enough to pay for. This sounds avoidable, but it catches a large number of businesses because owners confuse interest with intent to purchase. People say they would buy something; far fewer actually do when it’s time to hand over money.

Market validation before launch, even at a basic level, significantly reduces this risk. That means finding paying customers, not just interested contacts, before committing significant capital or time.

3. Weak or No Marketing Strategy

A business that doesn’t make itself visible to the right audience at the right time will struggle regardless of the quality of its product or service. This is particularly common among businesses founded by people with strong technical or trade skills who underestimate the time and resources required to generate consistent new customer enquiries.

For most UK SMEs, digital marketing is now the primary channel for customer acquisition. That includes search visibility, social media, email, and the quality of the business website. A business that has none of these working effectively is operating at a structural disadvantage. Our digital marketing strategy guidance covers how to build a channel mix that matches your business type and budget.

4. Lack of Strategic Planning

Businesses that operate without a plan tend to react rather than act. Without clear goals and a framework for decision-making, owners spend time on activity rather than progress. This is especially visible when an unexpected challenge arrives: a major customer leaves, a competitor undercuts on price, or costs rise sharply. Businesses with a plan know what to do. Those without one improvise, often badly.

A business plan doesn’t need to be a lengthy document. It needs to answer: who are your customers, how will you reach them, what does it cost to serve them, and how does the business grow? Those four questions, answered honestly, are worth more than a polished 40-page document that gets filed and forgotten.

5. Management and Leadership Gaps

Poor management is cited consistently in UK insolvency data as a contributing factor in business failure. This includes inexperienced decision-making, failure to delegate effectively as the business grows, and a lack of basic financial literacy among founders who built the business on technical or trade expertise rather than commercial skills.

Management capability is learnable. The businesses that grow past the early years are usually the ones where the founder has actively sought out the skills they’re missing, whether through formal training, mentoring, or bringing in people who complement their weaknesses.

6. Underestimating Competition

Competitors who are better funded, better positioned in search results, or who have been serving your target market for longer will take business from you if you haven’t thought carefully about your differentiation. This is particularly true in commoditised markets where price is the main variable.

Knowing your competitive position means understanding not just who your direct competitors are, but how they acquire customers, what their pricing looks like, and where their weaknesses are. For most SMEs, local SEO and a strong web presence are the most cost-effective ways to compete with larger, better-resourced businesses in their geographic market.

7. Failure to Adapt to Change

Businesses that were successful for years can still fail if they don’t respond to changes in their market: new technology, shifting customer expectations, or new competitors entering with a different model. This is less common in early-stage failure and more common in businesses that have been operating for five or more years and have stopped paying attention to where their market is moving.

The pattern looks similar across sectors: a business becomes comfortable with what works, stops investing in new capabilities, and doesn’t notice the ground shifting until it’s already lost significant market share.

UK Failure Rates by Industry

Not all industries carry the same risk. ONS business demography data identifies consistent patterns in which sectors see the highest closure rates.

| Sector | Primary Failure Drivers |

|---|---|

| Construction | Cash flow gaps between project completion and payment; subcontractor dependency |

| Accommodation and food service | High overheads, seasonal revenue, thin margins, high staff turnover |

| Information and communication | Rapid technology change; high competition from larger players |

| Professional, scientific and technical | Difficulty securing and retaining clients; high operating costs |

| Shift to online competition; high fixed costs, and footfall dependency | High overheads, seasonal revenue, thin margins, and high staff turnover |

| Retail | Shift to online competition, high fixed costs, and footfall dependency |

Construction and hospitality consistently show the highest failure rates. Both sectors combine tight margins with unpredictable cash flow, making them especially vulnerable to late payment and volume fluctuations.

For Northern Ireland specifically, the accommodation and food service sector is a significant part of the economy relative to its size, and the failure rate in this sector has been particularly visible since 2020. Businesses in these sectors need stronger cash reserves and tighter financial controls than those in lower-risk sectors.

How Digital Presence Affects Survival Rates

This connection is underrepresented in most discussions of business failure, but the evidence is clear: businesses with a strong, well-maintained digital presence survive at higher rates than those without one.

The mechanism is straightforward. A business that generates consistent leads through its website, Google Business Profile, and organic search is less dependent on any single customer relationship or referral channel. When one source of business dries up, others compensate. Businesses that rely entirely on word-of-mouth or a small number of large customers have almost no resilience when something goes wrong.

For Belfast and Northern Ireland SMEs specifically, investing in web design and SEO early creates a lead generation asset that compounds over time. A well-built website ranking for local search terms doesn’t stop working when you’re not in the office. Word of mouth does.

“The businesses we work with that are most resilient aren’t necessarily the ones with the best product. They’re the ones that have multiple ways for customers to find them and a consistent process for following up,” says Ciaran Connolly, founder of ProfileTree.

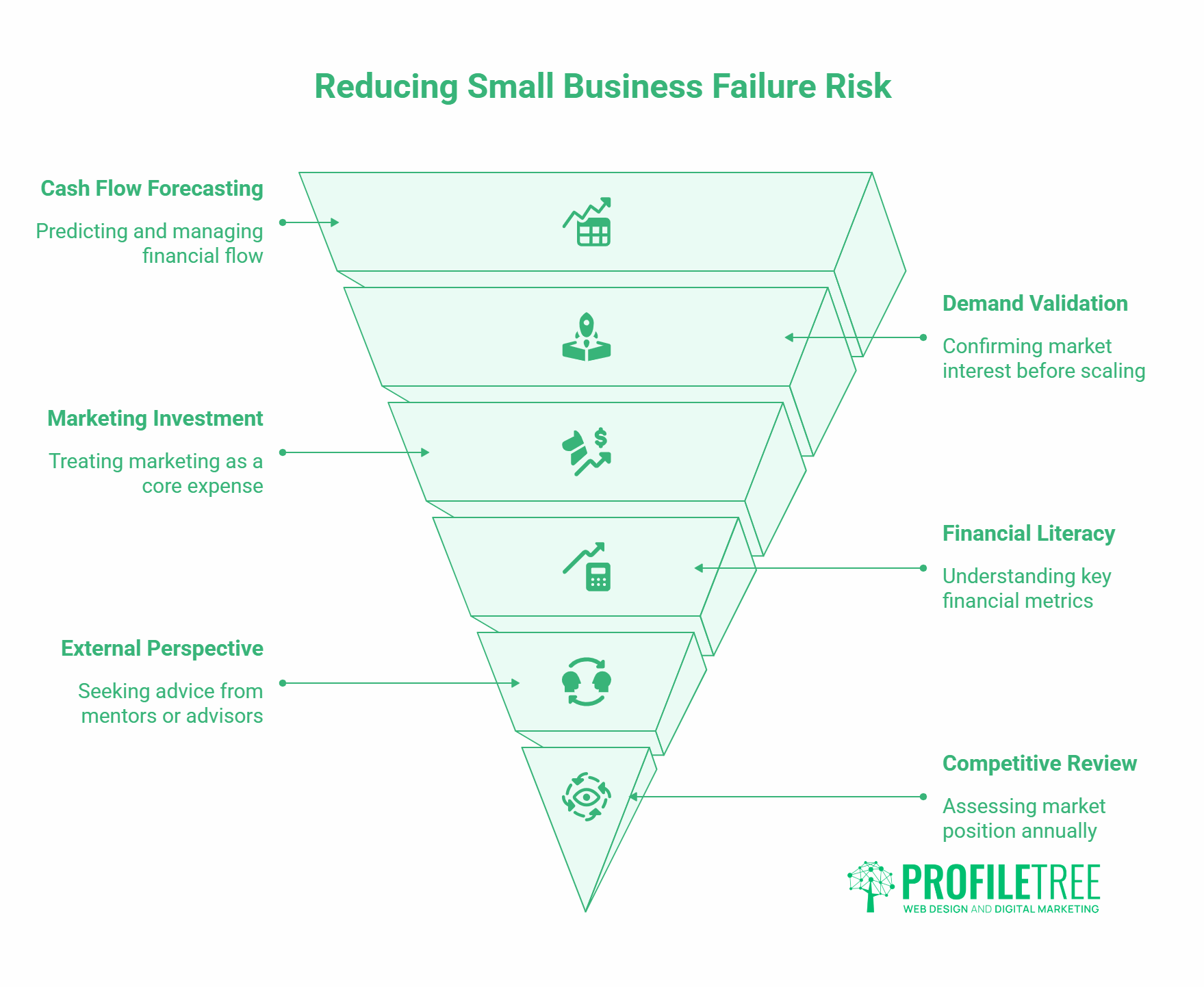

Practical Steps to Reduce Your Failure Risk

These steps address the causes listed above directly. None are complicated, but most require consistency over time rather than a one-time effort.

- Build a cash flow forecast and maintain it. A spreadsheet showing expected income and outgoings for the next 90 days, updated weekly, is one of the highest-value activities a business owner can do. It turns cash crises from surprises into visible problems you can address in advance.

- Validate demand before you scale. If you’re launching something new, find paying customers before you invest heavily in production, stock, or marketing spend. Revenue is validation. Interest is not.

- Treat marketing as infrastructure, not an optional extra. Allocating consistent budget and time to marketing, including your digital presence, is as much a survival requirement as paying your suppliers. Businesses that cut marketing first when money gets tight typically accelerate their own decline.

- Know your numbers. Gross margin, monthly burn rate, customer acquisition cost, and average customer lifetime value are the four numbers that matter most for most SMEs. If you can’t state them without looking them up, that’s a gap worth closing.

- Get an outside perspective early. The pattern in business failure is that problems are visible from the outside long before the owner acknowledges them internally. A mentor, an accountant, or an advisory board catches these problems earlier. The Federation of Small Businesses offers mentoring support for UK SMEs.

- Review your competitive position annually. Markets change. Competitors change. What worked three years ago may not be the right strategy today. A structured annual review of your positioning, pricing, and acquisition channels takes a day and is worth significantly more than that.

Support Available for UK and Northern Ireland Small Businesses

The UK has a well-developed network of business support, though many SME owners are unaware of what’s available to them.

- British Business Bank provides information on financing options, including start-up loans, growth finance, and government-backed schemes.

- Federation of Small Businesses (FSB) offers legal and financial advice, networking, and advocacy. Membership-based with a significant Northern Ireland presence.

- Invest NI supports Northern Ireland businesses with growth finance, export development, and business improvement programmes. Particularly relevant for businesses looking to scale beyond the local market.

- InterTradeIreland supports cross-border trade and business development for businesses in Northern Ireland and Ireland.

- Local enterprise partnerships and councils often run business start-up programmes, mentoring, and in some cases, grant funding for qualifying businesses.

Frequently Asked Questions

What percentage of small businesses fail in the UK?

Around 20% of new UK businesses close within their first year, based on ONS business demography data. By year five, approximately 50% have ceased trading. These rates have remained broadly stable for over a decade.

What is the most common reason small businesses fail in the UK?

Cash flow problems are the most common immediate cause of business failure, including among businesses that are profitable on paper but run out of working capital. Lack of genuine market demand and insufficient marketing are the next most common causes.

Do small businesses in Northern Ireland fail at the same rate as the rest of the UK?

Northern Ireland’s business survival rates track closely with the UK average. The economy has a higher proportion of micro-businesses, which face sharper cash flow pressures. Specific support from Invest NI and InterTradeIreland gives Northern Ireland businesses some advantages not available elsewhere in the UK.

Which industries have the highest failure rate in the UK?

Construction, accommodation and food service, and the information and communication sectors consistently show the highest failure rates in ONS data. These sectors combine tight margins with unpredictable cash flow and high competition.

Does having a website or digital presence improve a small business’s chances of survival?

Yes. Businesses with consistent digital lead generation are less dependent on any single customer or referral source, making them more resilient when one channel underperforms. SEO, Google Business Profile optimisation, and a well-built website create compounding returns over time that word-of-mouth alone cannot replicate.

What support is available for small businesses at risk in the UK?

The British Business Bank, FSB, and local enterprise partnerships offer financing guidance, mentoring, and advisory support. In Northern Ireland, Invest NI and InterTradeIreland provide additional programmes for businesses looking to grow or access new markets.

Is it possible to predict whether a small business will fail?

Not with certainty, but the risk factors are well understood: poor cash flow management, weak demand validation, no marketing strategy, and inexperienced management are present in the majority of failures. Addressing these proactively is the most reliable way to improve the odds.